When discussing the foundations of modern economics, the name Alfred Marshall deserves special recognition. Born on 26 July 1842, in London, England, Marshall became one of the most influential economists of the late nineteenth and early twentieth centuries. Although many people may not recognize his name today, his ideas continue to shape how economics is taught and understood around the world.

Marshall studied mathematics at the University of Cambridge, where he later became a professor. His strong analytical background helped him apply scientific methods to the study of economics. At a time when economics was still developing as an academic discipline, Marshall played a crucial role in transforming it into a more systematic and accessible field of study.

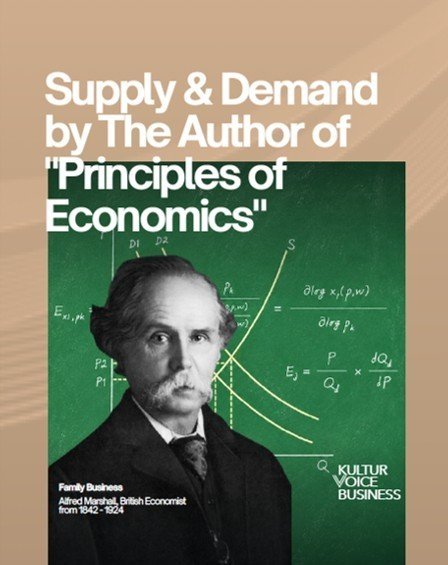

One of Marshall’s most significant contributions was his work on the theory of supply and demand. While the concepts of supply and demand existed before his time, Marshall refined and popularized them through clear explanations and graphical representations. His famous supply and demand curve demonstrated how prices are determined through the interaction between producers and consumers. This model remains one of the most fundamental concepts taught in economics classrooms today.

In 1890, Marshall published his masterpiece book, Principles of Economics. The book quickly became one of the most important economics textbooks in England and remained the standard reference for many years. Through this work, Marshall introduced key concepts such as price elasticity of demand, consumer surplus, and the distinction between short-run and long-run market behavior.

The book – Principles of Economics – is structured into six parts, which are Preliminary Survey (defining the substance and scope of economics, its evolution as a social science, and the order and aims of economic studies), Some Fundamental Notions (Establishes essential economic definitions, differentiating between wealth, capital, income, production, and consumption), Wants and Their Satisfaction (the foundation of demand, introducing the concepts of utility, marginal utility, and consumer demand, that Marshall famously detailed the Law of Demand and the Elasticity of Wants), The Agents of Production (supply side, discussing land and the law of diminishing returns), labor, population growth, industrial training, the accumulation of wealth), General Relations of Demand, Supply, and Value (introducing the famous “Marshallian Cross,” illustrating how market prices and output are determined simultaneously by the intersection of supply and demand curves, much like two blades of a pair of scissors), The Distribution of the National Income on how the total national wealth is distributed among the agents of production. It covers wages (earnings of labor), interest on capital, profits, and rent of land.

These ideas provided economists with valuable tools for analyzing markets and understanding economic decision-making.

Marshall believed that economics should not only explain how markets function but also contribute to improving society. He viewed economics as a practical discipline that could help address issues such as poverty, employment, and economic welfare. His focus on balancing theoretical analysis with real-world applications made his work highly influential among both academics and policymakers.

The legacy of Alfred Marshall extends far beyond his lifetime. His theories laid the groundwork for modern microeconomics and influenced generations of economists who followed him. Even today, students, researchers, and policymakers continue to rely on concepts that Marshall developed more than a century ago. Through his pioneering work on supply and demand and his influential writings, he helped shape the way the world understands economics.

Over the next two decades after he launched the book Principles of Economics, he worked to complete the second volume of his Principles, but his unyielding attention to detail and ambition for completeness prevented him from mastering the work’s breadth. The work was never finished and many other, lesser works he had begun work on – a memorandum on trade policy for the Chancellor of the Exchequer in the 1890s, for instance – were left incomplete for the same reasons.

The outbreak of the First World War in 1914 prompted him to revise his examinations of the international economy and in 1919 he published Industry and Trade at the age of 77. This work was a more empirical treatise than the largely theoretical Principles, and for that reason it failed to attract as much acclaim from theoretical economists. In 1923, he published Money, Credit, and Commerce, a broad amalgam of previous economic ideas, published and unpublished, stretching back a half-century.

Success in business rarely comes from luck—it’s built through consistent decisions and sharp thinking. If you want to refine your strategy and avoid costly mistakes, explore more business insights on KVB.global. Share this with your peers and follow Kultur Voice Business or KVB to stay aligned with ideas that drive real progress.

Latest news from Kultur Voice Business